In the near future, the rates, income limits and asset thresholds of Age Pension provided by Centrelink will be changed. Such reforms will have an impact on the number of older Australians who receive a full or a part pension and their eligibility. It is possible to understand them now and be able to budget, protect your entitlements, and come out not surprised in the next two weeks.

What Is Changing amongst Age Pensioners?

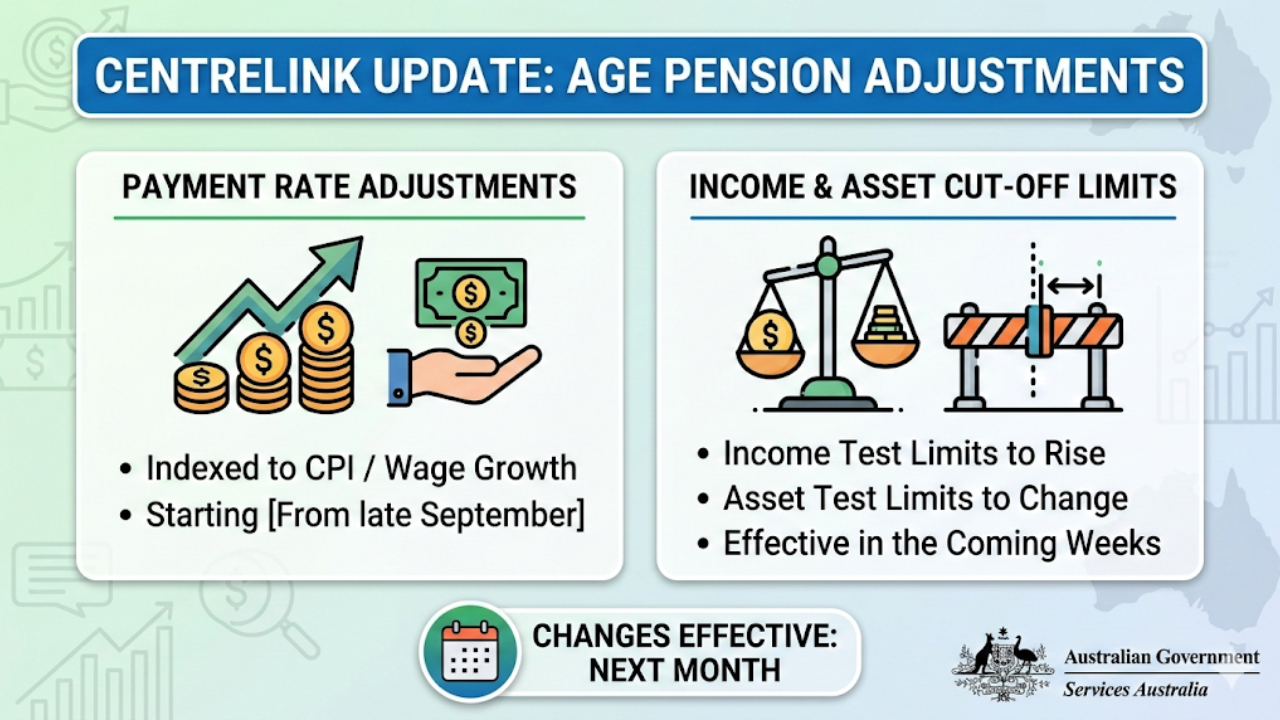

The age pension indexation is done after every march and September to keep up with changes in the cost of living and wages. The following bulk of increments comes in the matter of weeks. The basic amount of pension, the income and asset level will increase after the next date of indexation.

To the majority, it will be a small rise in the amount paid out every fortnight and greater tax-free capacity to earn or accumulate assets prior to the shrinking of the pension. Increased deeming rates on financial assets may however affect some pensioners so that their assessed income will rise and reduce the pension.

Bi-monthly Age Pension rates will rise both in single and couples.

Cut-off Limits in terms of income testing will increase giving additional income before checking cease installments.

Asset test requirements will be removed on both homeowners and non-homeowner.

Interest rates charged on savings and investments will increase.

New Rates of payments and How they operate.

The Age Pension is a flat rate income in retirement that is provided when you reach qualifying age which is 67 in the case of new claimants. The next upward indexation will raise the maximum rate of payment to the qualified pensioners by a small margin which will be automatically credited to their nominated bank accounts.

When you get a full pension, a slight increment should be reflected in your following payment after the date of change over without the need of making new claims. Part pensions recipients could also be affected particularly to those who are near the present cut off points since the increased thresholds are able to retain part or all of their benefits.

The amount is usually paid out every fortnight in your bank account.

The increments are automatic in case you are already qualified on the test date.

With the update, still your rate is based on the income and assets tests.

Limitates of Income and Asset: What You Can Have.

Centrelink applies a combination of two tests that are the income test and assets test and uses the test to have the lowest payment. Under the changes that are going on, you will have increased amounts of income and assets that you can earn and hold before losing all your pension.

According to the income test your payment is progressively less than the amount of your income which exceeds some free amount until you have reached the cut-off point and no longer qualifies. The assets test operates likewise; as soon as your assets have more than a set limit, the amount you will pay is reduced, and no more is paid, although the upper cut-off point remains constant.

There is income in employment, part of super withdrawals and deemed return of financial assets. The assets are savings, investments, cars and houses -regardless its principal house is exempt.

Increasing cut-offs will ensure that some individuals who were on the brink of losing their pension will not lose it.

Table of examples: revised settings in summary.

| Setting | Single (homeowner) | Couple combined (homeowners) |

|---|---|---|

| Maximum Age Pension (per fortnight) | Increases slightly from current level to a higher indexed amount. | Each partner’s maximum rate rises by a smaller but still positive amount. |

| Income cut‑off limit (per fortnight) | Higher income cut‑off so you can earn more before pension stops.finance.yahoo+1 | Combined cut‑off rises, allowing more shared income before losing eligibility.finance.yahoo+1 |

| Assets test upper cut‑off | Asset limit for a part pension moves up, giving more room to hold savings and investments.finance.yahoo+1 | Homeowning couples’ asset cut‑off increases, so more couples keep at least a part pension.finance.yahoo+1 |

| Deeming rates on financial assets | Lower deeming tier rises to 1.25%, higher tier to 3.25% from March. | Same deeming structure applied to combined financial assets of the couple. |

The Rates on Which You Should Judge.

Deeming rules presume the earning of your financial assets by a specific rate of return, what you actually earn. Income test involves this deemed income. Since the next date of change is the 1 background the lower deeming rate will increase to 125 percent and the higher rate to 325 percent, which was a time of rate stagnation.

In case you have bank accounts containing money or term deposits or shares or any superannuation account(s), the increase in deeming rates may affect the income assessed on you and decrease your pension. To most pensioners however, the effect of the increase in deeming must be much compensated by the increase in the rate of pensions and the increase of cut-off limits.

The deeming considered in most of the financial investments does not include your home and furniture.

The way to invest can still be up to you. Centrelink is driven by the deemed income.

Options are explicated safely by a financial advisor or a service such as the Financial Information Service.

The Preparation and Protection of your Entitlements.

Speaking of a number of moving elements, payment rates, income limits, asset thresholds and deeming, it is prudent to examine your circumstances prior to the commencing of the new regulations. Reviewing your current revenue, property and cash flow (including downsizing or increasing an amount out of super) may demonstrate that you may either switch to half or entire compensation, or the opposite.

To remain aware and secure rely on the government information and take care of fraudulent offers that claim to unlocked additional pension with use of risky schemes. When in doubt, you could speak directly with Centrelink, qualify with a licensed financial adviser or refer with respectable community and seniors organisations.

Check your Centrelink online account or letters to move up or down rates and thresholds.

Maintenance of income and asset records Current information To prevent the occurrence of overpayment or debt.

Consult experts separately to make significant financial adjustments to pursue a more substantial pension.

FAQs

Q1: Do I have to re- claim to receive a higher rate of Age pension?

A: No. In case you are already entitled on the change day, the new rate will automatically apply on your current payment.

Q2: Will an increase in the deeming rate cut down my retirement?

A: Yes. An higher deeming rate can boost the assessed income and reduce your pension but you will find that this will be offset by higher rates and levels.

Q3: Where can I find the specific new limits in my situation?

A: You would be able to access current income and asset details and details on deeming on official government websites or by directly calling Centrelink.